Checking your credit card statement is not the highlight of anyone's month, but it should still be done. In January 2021, Finder's Consumer Sentiment Tracker found that 17% of credit card holders admitted to not checking their statements at least once in that past year.

But it's important to understand how to read your credit card statement in order to keep track of your spending, make timely repayments, and flag any errors. Since most companies use a similar layout, we'll show you how to understand your credit card statement and what you need to pay attention to.

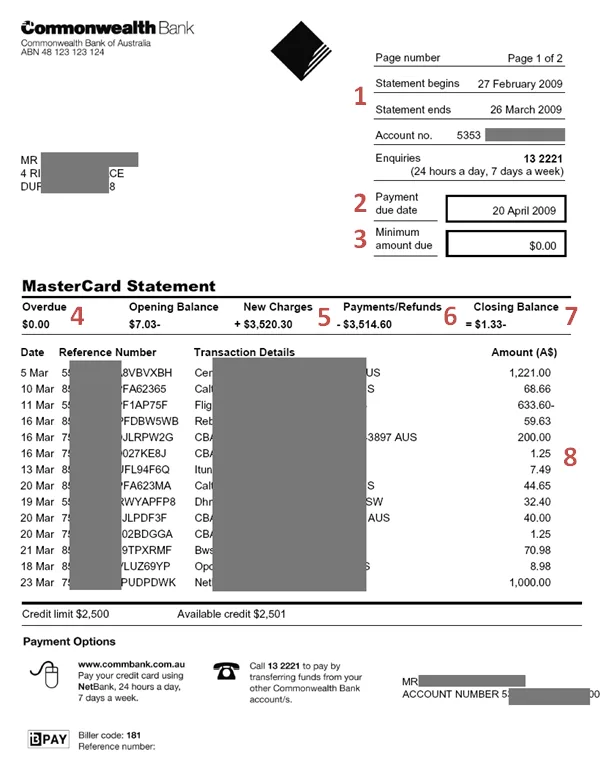

Key features on your credit card statement

Below we've outlined the major features of a credit card statement. We've numbered each feature to match this example statement to help you find these details on your own paperwork.

1. The statement period

Your statement period is usually listed in the top right-hand corner of your statement. If you wish to make use of your card's interest-free days, understanding your statement period can help.

One common mistake many people make is assuming that interest-free days apply from the date of the purchase. While credit cards offer up to X number of interest-free days, the exact number of days depends on your statement cycle and when you make the purchase.

Example: Let's assume that your card provides up to 55 interest-free days and the statement period is from 27 February to 26 March. The interest-free period for this statement period would end on 23 April. In this example, if you make a purchase on 27 February, you can make use of 55 interest-free days. If you make a purchase on 26 March, you get 28 interest-free days.

2. Payment due date

You can also find the payment due date on the top-right hand corner of your statement. This is the date you need to have made at least the minimum repayment by. You can pay the minimum or more before this date, but you'll be charged a late fee if you pay it after. Paying after your due date can also leave negative marks on your credit score, which could impact your chances of approval if you apply for another card in the future.

If you're having trouble paying your bill by that specific date, you can request to move the due date. For example, you might prefer that it falls shortly after your payday. If you're just struggling to repay that month, you can also request an extension. Most banks offer financial hardship assistance, so contact your card issuer directly to discuss your options.

3. Minimum amount due

When using a credit card, you must pay a minimum amount each month. The minimum repayment is usually between 2-3% of your outstanding balance. Otherwise, a dollar amount between $10 and $30 may apply if the balance is larger.

If you pay less than the minimum repayment, you could be fined. While you're obligated to meet the minimum, it's ideal that you pay as much as you can each month. If you only pay the minimum amount, it'll take longer for you to pay off your balance in full. The longer it takes you to pay off your balance, the more interest you will pay on what's already owed.

4. Overdue

If you've paid your bill late or paid less than the minimum, the amount you're yet to repay will be detailed in the "overdue" section of your statement. The longer you have an overdue account, the more you'll be charged in late payment fees.

Overdue credit card bills collect fees and interest that increases your debt. It can also hurt your credit score. Overdue statements are a red flag to lenders and could reduce your likelihood of approval for future loans and cards.

5. New charges

This is a summary of the total amount of money charged to the card during the statement period. Look at the new charges to make sure the total amount matches up with the transactions that you've made. This can help ensure there aren't any errors on your statement (such as fraudulent transactions or double charges).

6. Payments/Refunds

This is the total of all the payments made towards the card, along with any refunds, during the given statement period. Some refunds can take a few weeks to process.

If you can't locate the refund on your statement, you might need to contact your bank or the organisation issuing the refund to make sure that it has gone through properly.

7. Closing balance

This amount refers to how much you owe on your credit card account in total. If you pay more than you owe, this figure goes into negative. While you're only obligated to pay the minimum repayment each month, you should aim to pay as close to the closing balance as possible. If you pay the closing balance in full, you can avoid interest. You may also qualify for up to a certain number of interest-free days on purchases.

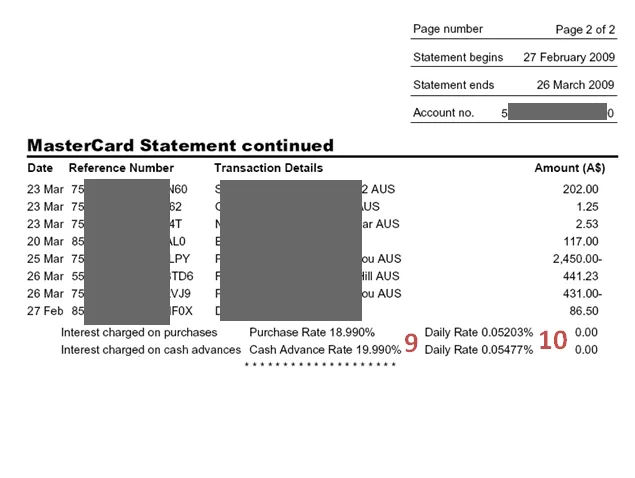

8. Transactions

This list will detail all of the transactions you've made on that card during that statement period. It should include the date of the transaction, its reference code, the type of transaction and the dollar amount.

Again, it's wise to look over your transaction history to make sure that you haven't been charged incorrectly or fraudulently in the previous statement period. Most credit cards also come with mobile apps which allow you to check your transaction history, so you won't have to wait for your statement to arrive to check these details.

9. Daily rate

While banks usually present the interest rate as an annual percentage, it's actually charged on your transactions on a daily basis. So you can use the daily rate to see how much your balance is collecting in interest each day, including your purchases, balance transfers and cash advances. Most transactions, aside from cash advances, usually don't start accruing interest until after the statement period ends, though.

10. Reward points

You can expect these details only if you use a rewards credit card or frequent flyer credit card. If you do, your statement should inform you of points earned during the statement period, the total number of points in your account, and points redeemed during this period. You can also monitor how many points you've earned through your online rewards program account and frequent flyer account balance.

How to manage errors on your credit card statement

While your credit card statement should usually be accurate, there are some instances where you might spot an error. If these errors go unreported, they could have a negative impact on your credit history and reduce your likelihood of approval when applying for future loans. This is why it's so important to keep an eye on your credit card statement.

If you do spot an error on your credit card statement, it's wise to get in contact with your card provider to report and resolve the issue. If you do this soon enough, the errors might not even make it to your credit file. The simple steps you can follow to report and fix an error on your statement include:

If you spot a purchase you’ve not made, contact your card provider immediately.

In some instances, the responsibility to prove you haven't made the purchase is on you, so make sure you have the relevant receipts and evidence on hand.

If you feel you’ve been a victim of identity theft or if your card has been used for fraudulent transactions, you should also contact the police as well as your provider. See our guide on how to survive credit card fraud for more tips.

If any such errors make it to your credit report, you’ll have to contact credit reporting bodies such as Experian, Dun and Bradstreet or Equifax individually to order a copy of your credit report. You can then get in touch with a credit repair agency to help clean up your credit report.

See our guide on how to lodge a credit card dispute with your bank for the contact details and steps you need to report an error on your credit card statement.

Your credit card statement might seem like just another bill to deal with at the end of every statement period, but it's important to look over it rather than just paying your bill each month. Understanding how your statement works will not only ensure that you make timely repayments and avoid collecting interest, but will also help you spot any errors on your statement and resolve them before they impact your credit file.

Frequently asked questions

Unfortunately, the answer to this is no. However, by doing so you can look forward to clutter-free space and you can also do your bit to save the environment. Most banks issue electronic credit card statements, so this might be an easier way to manage your statements.

Credit card providers in Australia issue statements on a monthly basis. Make sure you contact your bank if you haven't received your credit card statement around the time you usually would in the month.

This might be because you have an outstanding balance in your account from the previous billing cycle. Bear in mind that you have to pay your account’s closing balance in full before each due date if you wish to take advantage of your card’s interest-free days.

All transactions are listed within one statement. As the primary cardholder, you're liable for any transactions made with any additional cards. This is why it's important to check your statement and keep track of all transactions being made.

Rebecca Pike is Finder's senior writer for money. She joined Finder after almost four years writing for business publications in the mortgage and finance industry, including three years as editor of Mortgage Professional Australia. She regularly appears as a money expert on programs like Sunrise and Today, as well as across radio and newspapers. She also holds ASIC-recognised certifications in Tier 1 Generic Knowledge and Tier 2 General Advice Deposit Products.

When you apply for a credit card online, you could receive a response within 60 seconds. Find out how you to find a card that you're eligible for and increase your chances of approval.

Your online statement will generally be the most accurate/ updated record and more reliable to pay to. It may be useful to check the payment records on the postal record and compare that to the online statement. There is a possibility that your credit card has had some pending or new transactions between the time your postal statement was mailed and when you have received it.

You will receive a statement a month after opening the account. If you want to keep track of purchases before a statement is sent out to you in the mail. You can check and manage your account online through your lender’s online banking facility.

Hi Christopher. Thanks for your question. Your credit card statement will show you all your transactions for the month. This includes purchases and cash advances. Statements come in the mail but you elect to receive them electronically. Jacob.

HI Marsha. Thanks for your question. You will need to pay all balances eventually if you want to get out of debt. But typically, the opening balance will have the card’s annual fee (if applicable) and any transactions you’ve made in the first month. You will need to make at least the minimum monthly repayment to stop your account from going in to arrears. Jacob.

How likely would you be to recommend finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Important information about this website

finder.com.au is one of Australia's leading comparison websites. We are committed to our readers and stands by our editorial principles

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product. You can learn more about how we make money.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

Hi, My Visa CC statement just arrived by post yet my online closing balance shows a lot less, which one should I pay?

Cheers, John

Hi John, thanks for your inquiry!

Your online statement will generally be the most accurate/ updated record and more reliable to pay to. It may be useful to check the payment records on the postal record and compare that to the online statement. There is a possibility that your credit card has had some pending or new transactions between the time your postal statement was mailed and when you have received it.

Cheers,

Jonathan

How can I know my credit card statement?

Hi Jaswant.

You will receive a statement a month after opening the account. If you want to keep track of purchases before a statement is sent out to you in the mail. You can check and manage your account online through your lender’s online banking facility.

Thanks for your question.

Do the things you purchase end up on your credit card statement?

Hi Christopher. Thanks for your question. Your credit card statement will show you all your transactions for the month. This includes purchases and cash advances. Statements come in the mail but you elect to receive them electronically. Jacob.

Is the opening balance the one you pay?

HI Marsha. Thanks for your question. You will need to pay all balances eventually if you want to get out of debt. But typically, the opening balance will have the card’s annual fee (if applicable) and any transactions you’ve made in the first month. You will need to make at least the minimum monthly repayment to stop your account from going in to arrears. Jacob.